Suppose that every day, ten men go out for lunch and the bill for all ten comes to $100. If they paid their bill the way we pay our taxes (including GST on purchases), it would go something like this:

So, that's what they decided to do. The ten men ate lunch in the restaurant every day and seemed quite happy with the arrangement, until one day, the owner threw them a curve ball. "Since you are all such good customers," he said, "I'm going to reduce the cost of your daily lunch by $20.00." So lunch for the ten men would now cost just $80. The group still wanted to pay their bill the way we pay our taxes. So the first four men were unaffected. They would still eat for free. But what about the other six men? How could they divide the $20 windfall so that everyone would get his fair share? They realized that $20 divided by six is $3.33. But if they subtracted that from everybody's share, then the fifth man and the sixth man would each end up being paid to eat his lunch. So the bar owner suggested that it would be fair to reduce each man's bill by a higher percentage the poorer he was, to follow the principle of the tax system they had been using, and he proceeded to work out the amounts he suggested that each should now pay.

Each of the six was better off than before. And the first four continued to eat lunch for free. But, once outside the bar, the men began to compare the amount they got off. The sixth man said, "I only got $1 off out of the $20 while the tenth man got $10 off!" "Yeah, that's right," exclaimed the fifth man. "I only got $1 off, too. It's unfair that he got ten times more benefit than me!" "That's true!" shouted the seventh man. "Why should he get $10 off, when I got only $2? The wealthy get all the breaks!" "Wait a minute," yelled the first four men in unison, "we didn't get anything at all. This new tax system exploits the poor!" The nine men surrounded the tenth and told him they were angry that he got so much off while they each got very little. The next day the tenth man didn't show up for lunch, so the nine sat down and had their lunches without him. But when it came time to pay the bill, they discovered something important. They didn't have enough money amongst all of them for even half of the bill! And that is how our tax system works. The people who already pay the highest taxes should naturally get the largest benefit from a tax reduction. Tax them too much, attack them for being wealthy, and they just may not show up anymore. In fact, they might start eating overseas (& there are a million and one instruments to avoid taxes), where the atmosphere is somewhat different (there is no such thing as a fair tax system)! Socialist ideals only works to provide for the bottom rung of Maslow's hierarchy of needs! Anything above that, everybody suffers making everybody poorer!...and most importantly kill innovation! examples abound from Cuba to China so unless you want be that, you've got to think harder about what you want! For those who understand, no explanation is needed. For those who do not understand, no explanation is possible. ~Sourced from the LSE think tanks

0 Comments

Introduction The purpose of this article is

CryptocurrencyA cryptocurrency is a medium of exchange like the USD, AUD, CAD etc but designed for the purpose of exchanging digital information through a process made possible by certain principles of cryptography. Cryptography is used to secure the transactions and to control the creation of new coins. The first cryptocurrency to be created was Bitcoin back in 2009. Today there are hundreds of other cryptocurrencies, often referred to as Altcoins. Put another way, cryptocurrency is digital currency. Unlike centralized banking, like the Federal Reserve System, where governments control the value of a currency through the process of printing fiat money, governments (or indeed any single or group of individuals or organisations) have no control over cryptocurrencies as they are fully decentralized. Most cryptocurrencies are designed to decrease in production over time like Bitcoin, which creates a market cap on them. That’s different from fiat currencies where financial institutions can always create more, hence inflation. Bitcoin will never have more than 21 million coins in circulation. The technical system on which all cryptocurrencies are based on was created by Satoshi Nakamoto (a pseudonym) While hundreds of different cryptocurrency specifications exist, most are derived from one of two protocols; Proof-of-work or Proof-of-stake. All cryptocurrencies are maintained by a community of cryptocurrency miners who are members of the general public that have set up their computers or ASIC machines to participate in the validation and processing of transactions. What problems do Cryptocurrencies solve?Before we launch into cryptocurrencies - it's important to briefly understand what problem (s) they actually solve! Principally, there are 2 key problems

Once there is understanding of the problems this trust causes, it is easy to see how cryptocurrencies remove these risk almost completely from commerce making transaction costs cheaper and accurate and the medium of to maintain value. To get to that, it is important to understand what really is currency, what is a bank, what is a government and what has all that to do with Faith or Trust? We do apologies in advance about the level of complexities in the concepts discussed. Given the brief scope of the article, the readers are expected to at least have an awareness of the existence and types of cryptocurrencies. CurrencyA currency is a physical note and coin issued by the government of a particular country as a medium of exchange to facilitate commerce and to some extent store of value in terms of purchasing power. It is a promissory note in which the issuer (the government) promises to give to the holder value in the denomination of that note! These are also called "Fiat Currencies" as they are created and backed solely by trust (or faith) in a integrity of the government that it will actually be able to deliver the promised value when it is presented by the holder. Bank A bank is an organisation that the people "trust" to

ProblemAs discussed in the introduction above, the key problem is Trust (or faith)

GoldProblem 1) wouldn't exit if the governments' ability to print currency (& therefore its promise) is backed up by inherent value holdings (eg in gold as in the olden days - called the Gold Standard)! Gold doesn’t inflate / deflate like fiat currencies do. Given its limited supply, it is guaranteed to hold its value. Things tend to cost the same in gold over long periods of time. In fact, 2,000 years ago, Roman centurions were paid about 38.58 ounces of gold per year. In US dollars today, this comes out to about $48,350. The base salary of a captain in the US army today comes out to just about the same at $48,500. This makes gold a much better store of value than fiat currency! You don’t have to trust anyone to trust that your gold will retain its value relatively well across the sands of time. The problem with gold though, is its' use as a medium of exchange! It is hardly practical to carry gold around and shaving the exact weight required for a cup of coffee or a taxi / bus ride or perhaps a dress or to transfer value over long distances. This precise problem drove the development of fiat currencies! How does Cryptocurrency solve the above problems?Cryptocurrencies solve both issues! Given the Gold analogy, a cryptocurrency is "Digital" gold so much so that its' extraction is even called mining! It is

As a business, what do you need to get setup to transact in cryptocurrencies?Well, generally speaking, as a business, in principle, you need to do the following steps to get setup up to transact in cryptocurrencies.

The complications arise in accounting & reporting for these transactions! Given they the sender and recipient are virtually anonymous on the decentralised records, their reporting becomes very complex. Recognition of whether a transaction is on revenue account (resulting in tax obligations) or capital account (Loans and advances) add further complications. Regulators are yet to catch up and understand the fundamental nature of cryptocurrencies. All their systems & understanding are based on traceability to sender / receiver and purpose as there is an audit trail of every transaction. Sooner or later regulations will come and if you're keen to stay on the right side of these, please come see us so we can configure your accounting systems and train accountants / business owners to deal with digital wallets. Aside from reporting end, at the business process level the application of blockchain technology is ushering in B2B connectivity at the General Ledger / Accounts Payable / Accounts Receivable / Stock / Fixed assets levels where creditor bills & debtor invoices and there subsequent settlement will happen at the accounting systems level without the need for duplication or time delays! If you need to know more about where the technology is headed - please check out : https://request.network/assets/pdf/request_whitepaper.pdf. What are the tax implications (as at the date of writing this article)?Cryptocurrencies are both a store of value (like gold) and a medium of exchange (like a $) and that itself creates a host of tax issues - one for settling transactions and then valuing the Bitcoins as there are literally hundreds of exchanges all over the world matching buyers and sellers! There is no official guidance from the IRD in relation to cryptocurrencies. Type in cryptocurrencies, Bitcoin, Ethereum, Dash, Ripple and so on, in the search box and you get absolutely nothing. We tried to connect with our account managers at the IRD and similar response! Without specific guidance from the IRD, for now we cannot imagine the treatment of cryptocurrencies to be any different from existing systems to measure & report transactions made in foreign currencies and foreign currency holdings. If a NZD transaction is settled in a fiat currency, we'd use one of the options (transaction date rate, rolling averages, mid-month rates etc.) to record settlement (& consequent profit or loss). Thereafter, we would revalue the holdings of foreign fiat-currencies at reporting dates based on rates published by the IRD - with the translation loss or gain being tax deductible or taxable as the case maybe. When it comes to Altcoins, there are literally hundreds of exchanges in the world where these are traded and a trader / holder is free to trade on any exchange without any artificial encumbrances at all! Transactions in Altcoins will pretty much follow the same methodology except that, in the absence of any publications from the IRD, we think using the closing period end value from a few prominent exchanges should do the trick as along as the same exchange is used every period end. It is important to note that there is no law or rule about it yet but we believe that this would be the position most easy to defend! Key message The key message here is that regardless of the simplicity of the concepts, its often not so simple to get setup for cryptocurrency payment gateways, link them to the general ledger integrations and work the taxable profits and losses from such transactions. We do recommend you contact us so we can discuss the details & specifics to your case before advising on the appropriate methodology going forward. Disclaimer

The above publication discusses business issues generally and is not intended to be specific advice. Whilst every effort has been made to provide valuable, useful information, Core Business Services Ltd, any related suppliers, associated companies & practices accept no responsibility or any form of liability from reliance upon or the use of its contents. Any suggestions should be considered carefully within your own particular circumstances, as they are intended as general information only. Please do consult with your advisor or call this firm for information / advise specific to your circumstances before finalising any particular course of action.  Recently a few new clients called to understand what type of entertainment expenses are deductible for tax purpose and what's not. Technically, expenses incurred in earning assessable income are deductible for tax purposes. Most business related expenses are fully deductible. If the expense doesn’t help your business earn gross income, it’s private and you can’t claim it as a tax deduction. A principle, easy enough to get, right? Well, it turns out that its not so simple in relation to some expenses. Given that its relatively easy to extend an argument in favour of a position one is taking, the IRD has specified some rules in relation to some of expenses - entertainment is one of them. This article discusses, with some examples what type of entertainment is deductible for tax purposes and what type is not. We have used examples of Christmas parties below as some shops & cafes have already started to get setup for Christmas parties! Deductibility also impacts GST & FBT so its important that one understands this carefully. EntertainmentIt becomes a little trickier when there’s an element of private enjoyment. You might think that the firm’s Christmas party for clients is a business related expense and should be fully deductible because it’s promoting your business, products or services.

Generally speaking, if there’s an element of private enjoyment, the expenses (in addition to the food and drink) associated with events where you entertain clients and/or staff will only be 50% deductible. For instance, this would include the hire of crockery, glasses, waiting staff and music. Accordingly, if your clients OR employees OR anyone associated with the business have a greater opportunity to enjoy the entertainment than the general public, you can only deduct 50% of the costs. There are exceptions of course! Entertainment supplied for charity is 100% deductible. For instance if you throw a Christmas party for the children’s ward at the local hospital, this is fully deductible. Entertainment enjoyed outside New Zealand is 100% deductible. If you take the team to Fiji or Cook Islands for Christmas (lucky them!), all costs (net of amounts contributed by staff if any) will be fully deductible.  Recently a few of our clients' staff were appointed to the board of companies acquired by the clients. We were approached by the staff to advise on their rights, duties and obligations as directors.

This article endeavours to discuss the essentials of being an effective director, whether you have been appointed by your employer to the board of one of its subsidiaries or you have accepted the role of the director in a company, even if you are one of its shareholders. We will discuss what the law sets out as your legal rights, duties and obligations and what they mean on a practical day-to-day basis. Being a director is more than just a title - they need to be both risk-managers and responsible risk-takers to enable companies to grow and survive. Directors are the representative of the company and shareholder, and answer to them. Even if you are also the main shareholder, as a director you’ll have legal responsibilities to actively monitor the management of your company and may face serious penalties if things go wrong. Although the article addresses directly the directors, the practical day-to-day conduct applies equally to trustees. ...So before you take up a directorship  What is my business / shares worth?Every business owner would like to know the true current market value of their business. Unfortunately, no single quick "rule of thumb' will help determine the true value of a business. In fact business valuations are performed in order to take the guess work out of valuing the business.

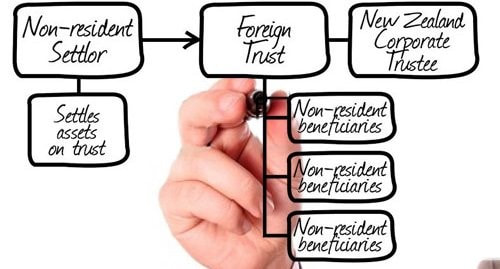

Although there are additional adjustments applied to value shares of closely held businesses to account for levels of control & influence over business decisions & marketability of the particular parcel of shares, for the purposes of this we will use the term business valuation to include valuation of shares as well.  What the different types of Trusts for Tax purposes?There are three types of trust for New Zealand income tax purposes:

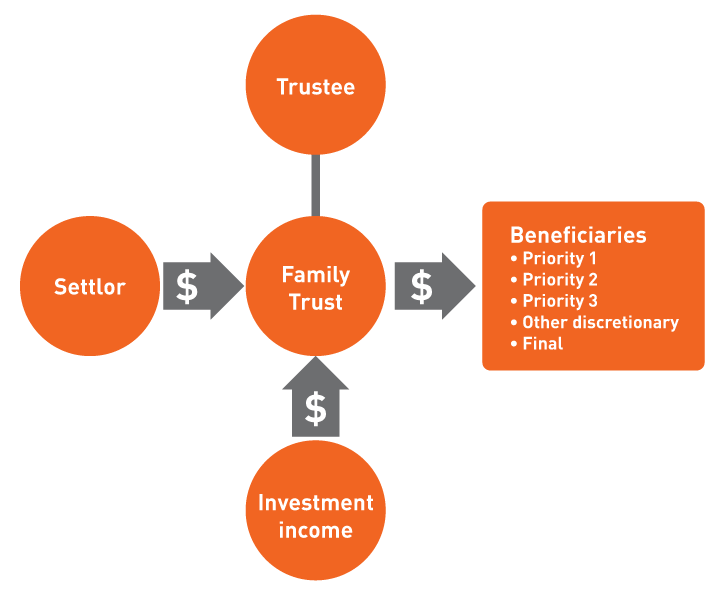

This article only deals with Foreign Trusts. What is a family trust? A trust exists when one person (a "trustee") holds and owns property for the benefit of another person (a "beneficiary"). A family trust is a trust set up to benefit members of your family.

The purpose of the family trust is to hold (through you transferring your assets), so that legally you own no assets yourself, and through the trust, still have some control over, and get the benefit of, these assets. You can set up a family trust either while you are still alive (by a declaration of trust contained in a trust deed) or when you die (by the terms of your will). This article is mainly concerned with trusts created while you are alive, and with the benefits that these trusts can provide for you in your lifetime. The family trust can be setup either as a "Fixed" trust (with named / specified beneficiaries with fixed ratio / amount of benefits) or a "Discretionary" trust (with "described" beneficiaries with benefits that are at the "discretion" of trustees). This is discussed in a bit more detail in the beneficiaries section below.  BackgroundMore and more companies are being re-organised by value chain (how the business adds value to its customers and stakeholders) rather than functionally (Products, production, finance, HR etc). Unfortunately management accounting has failed to keep pace in delivering value added proactive periodic financial reports!

This is particularly true in small to medium sized organisation (both for and not-for-profit sectors) where traditional accounting is used mostly as part of its compliance infrastructure. Among other disadvantages, this approach

Incorporating the portfolio approach to management reporting insures that

Although the concepts, in different incarnations, are applicable to both new and existing businesses, it is particularly beneficial to those at the cusp of a growth spurt.  BackgroundIn October 2015, the National Government introduced the Bright Line Test on land transactions. This was an attempt to slow down the runaway property market by imposing extra "costs" on land transactions that fall within the ambit of the Bright Line Test!

The government didn't really have a choice - the dreaded Capital Gains Tax is political suicide and the runaway property prices was hurting the government's chance for re-election (oh yes! & the public). So, quite brilliantly, they applied what is common in some European countries. It is obviously working as CoreLogic data shows that 7% of the Auckland sales in 2016 were properties that were sold within a year compared to 11.7% at the peak of the last boob during mid-2000.  Withholding Tax (or TSP) is like PAYE for certain type of contractors. This was more or less a flat rate earlier. From 1 April 2017, 2 key things have changed:

What is a schedular payment?Schedular payments are payments made to contractors who perform certain activities. These payments are required to have tax deducted but they’re different to salary or wage payments.

Schedular payments apply to contractors across a broad spectrum of industries; from cleaners, farm workers and gardeners, to entertainers, sportspeople, labour-only builders and fishing boat workers. Details of what type of payments can be considered is included in the IRD form IR330C. |

AuthorCORE Business Services Archives

September 2021

Categories |

RSS Feed

RSS Feed